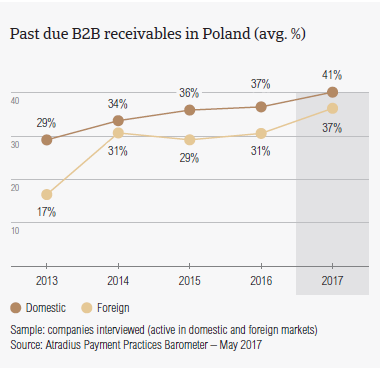

Overdue B2B invoices occurred more often with the domestic customers of our Polish respondents (41.0%) than with their foreign customers (36.6%).

Polish GDP growth has slowed since 2015 due to a fall in investments. In 2017, GDP is forecast to reach 3.3%, up from 2.8% in 2016. While investments are recovering, they continue to be hampered by political uncertainty and increasing insolvencies.

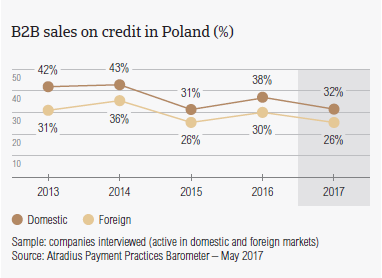

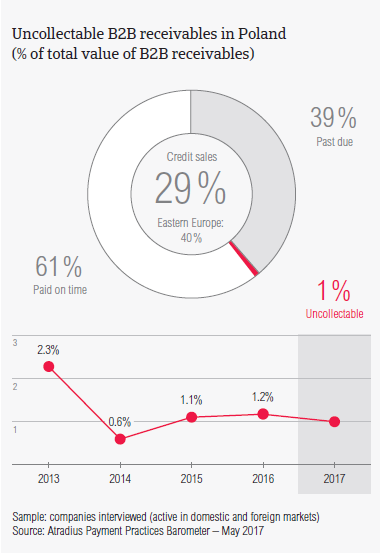

Sales on credit terms

After a modest increase from 28.1% in 2015 to 33.9% in 2016, the percentage of sales on credit terms decreased again this year (28.9%). Among the Eastern European countries surveyed, Poland is one of the least inclined countries to sell on credit terms.

- On average, 32.0% of the sales to domestic B2B customers were made on credit. This highlights a year-on-year decrease of five percentage points. In respect to Polish respondents’ foreign B2B customers, on average, 25.7% of transactions was made on credit (down from 30.3% in 2016).

- Like in 2016, the proportion of B2B sales on credit in Poland (28.9%) is far below that of Eastern Europe overall (39.8%).

- Polish respondents’ aversion to selling on credit is slightly more focused on foreign (25.7%) than on domestic transactions (32.0%). Past surveys showed the same reluctance.

- The higher percentage of sales on credit to domestic customers may reflect more familiarity with domestic business practices and a higher level of trust when dealing with compatriots.

Overdue B2B invoices (%)

The percentage of overdue B2B invoices in Poland continued its upward trend. Despite an increase of five percentage points, the percentage of overdue B2B invoices in Poland (38.8%) is lower than the regional average (41.5%).

- A higher percentage of respondents in Poland (89.2%) reported late payments of B2B invoices than in the rest of the Eastern European countries surveyed (83.7%).

- On average, late payments to Polish respondents occur just as frequently from domestic B2B customers as they do from foreign B2B customers (89.2%). Moreover, among the Eastern European countries surveyed, Poland reported the highest frequency of late payments by foreign B2B customers (89.2%).

- Overdue B2B invoices occurred more often with the domestic customers of our Polish respondents (41.0%) than with their foreign customers (36.6%). Both these averages are lower than those registered in Eastern Europe overall (domestic: 45.2%; foreign: 37.7%).

- The Days Sales Outstanding (DSO) figure in Poland is 88 days (up from 71 days in 2016). This is also 27 days longer than the DSO figure in Eastern Europe overall.

- Looking ahead, 57.6% of Polish respondents said that they do not expect changes in their annual DSO figure in the coming 12 months. However, 23.0% foresee a slight increase and 12.2% expect a slight decrease.

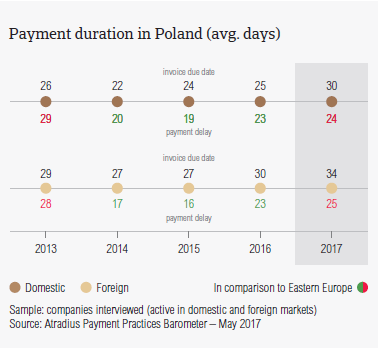

Payment duration (average days)

Like most of their peers in Eastern Europe (with the exception of Turkish respondents), in 2017, respondents in Poland granted more relaxed payment terms to both their domestic and foreign B2B customers.

- In 2017, domestic B2B customers of respondents in Poland were given, on average, 30 days from the invoice date to settle their invoices. This is five days longer than the average domestic payment term in 2016.

- Another increase was observed with average payment terms granted to foreign B2B customers. Polish suppliers granted, on average 34 days for invoices to be paid, four days more than in 2016.

- Despite offering more time for invoices to be paid, respondents in Poland reported minor increases in payment delays. Domestic B2B customers delayed their payments, on average, by 24 days (up from 23 days in 2016). Foreign B2B customers delayed payments, on average, by 25 days (2016: 23 days).

- In 2017, suppliers in Poland need to wait 56 days (six days more than in 2016) to convert B2B receivables into cash. This is the second longest credit to cash turnaround period of the Eastern European countries surveyed.

Key payment delay factors

Insufficient availability of funds was the most frequently mentioned reason for payment delays in Poland and in Eastern Europe overall.

- 63.1% of Polish respondents cited liquidity concerns as the primary reason for payment delays by their domestic B2B customers. This compares to a lower percentage of 58.4% in Eastern Europe overall.

- Looking at payment delays by foreign B2B customers, 31.4% of Polish respondents said that delays occurred mainly because of the complexity of the payment procedure. This differs from the most frequently cited reason at regional level (liquidity concerns: 33.6%).

- A second most cited reason for payment delays was the buyers’ use of outstanding invoices as a form of financing, stated by 33.9% for domestic and 24.5% for foreign B2B customers of respondents in Poland. Eastern Europe showed a similar picture (domestic: 32.4%; foreign: 27.7%).

- 43.5% of Polish respondents said that payment delays did not have a significant impact on their businesses. However, 23.9% said that due to late payments they needed to postpone payments to their own suppliers and 17.4% that they needed to pursue additional financing from banks, factors and others.

Protection of business profitability

Slightly fewer respondents in Poland (11.5%) than in Eastern Europe overall (13.1%) stated their intention to do more to protect their businesses from the impact of Brexit, the slowdown in Asia and US protectionism.

- 53.8% of respondents in Poland said that in the face of the above-mentioned developments, they are most likely to maintain their current mix of credit management tools. This percentage is in line with the one expressed in Eastern Europe overall (53.3%).

- When asked about which credit management actions they are most likely to increase their use of, Polish respondents stated that they would increase checks on their buyers’ creditworthiness (14.2%) and increase bad debt reserves (13.8%).

- Despite the UK being their second largest export market, the impact of Brexit doesn’t seem to concern Polish respondents. Only 14.9% of respondents in the country said that they will increase creditworthiness checks on their buyers and 14.7% said that they will increase bad debt reserves to strengthen current credit management.

- To manage risks arising from US protectionism, 16.2% of Polish respondents said that they will increase monitoring of their buyers’ credit risk while 15.0% said that they will increase bad debt reserves and creditworthiness checks on their buyers.

- The slowdown in Asia seems to be the least likely to prompt Polish respondents to increase protection and use of credit management tools.

Uncollectable receivables

The total value of B2B receivables written off as uncollectable in Poland decreased slightly from 1.2% in 2016 to 1.0% in 2017. The same decrease was noticed at regional level, where the percentage of uncollectable B2B receivables also stands at 1.0%.

- Uncollectable receivables in Poland consisted almost entirely of domestic write-offs (domestic: 0.8%; foreign: 0.2%).

- Polish respondents reported that in 2017 the largest proportion of uncollectable receivables came from these sectors: construction, consumer durables, food and business services.

- 50% of Polish respondents surveyed said that B2B receivables were written off as uncollectable because of the customers’ bankruptcy. 25.9% of respondents said that this occurred because the cost of pursuing debts was too high while 23.2% said write-offs were a result of failed collection attempts.

Payment practices by industry

24.0% of respondents in Poland said that they expect an overall deterioration in the payment behaviour of their B2B customers over the coming 12 months. This percentage is slightly lower than that of Eastern Europe overall (26.0%) and the second highest in the region after that of Turkey (50.0%).

- Invoice payment terms extended by Polish respondents to B2B customers in the construction industry (38 days) and the machines sector (39 days) are significantly longer than the country average of 32 days.

- The shortest payment terms were given to B2B customers in the textiles industry (14 days).

- Despite lenient payment terms, B2B customers of respondents in the construction sector settled overdue payments the slowest. 51% of Polish respondents said that payment delays were mostly a result of insufficient availability of funds and 42% said that delays occurred because of their buyers’ use of outstanding invoices as a form of financing.

- Around 24% of Polish respondents expect a worsening of payment practices over the coming 12 months. This is significantly more than the percentage of respondents who said that they anticipate improvement (13%).